A rise in lending to the retail sector could render the banking system vulnerable, after it has just overcome its NPA problem.

A renewed focus on retail lending, or the provision of personal loans, by India’s banking system (and the non-bank financial companies they support), is giving the otherwise confident Reserve Bank of India some cause for concern. That the period after pandemic year 2020-21 has witnessed a spike, if not boom, in retail credit is clear from the evidence.

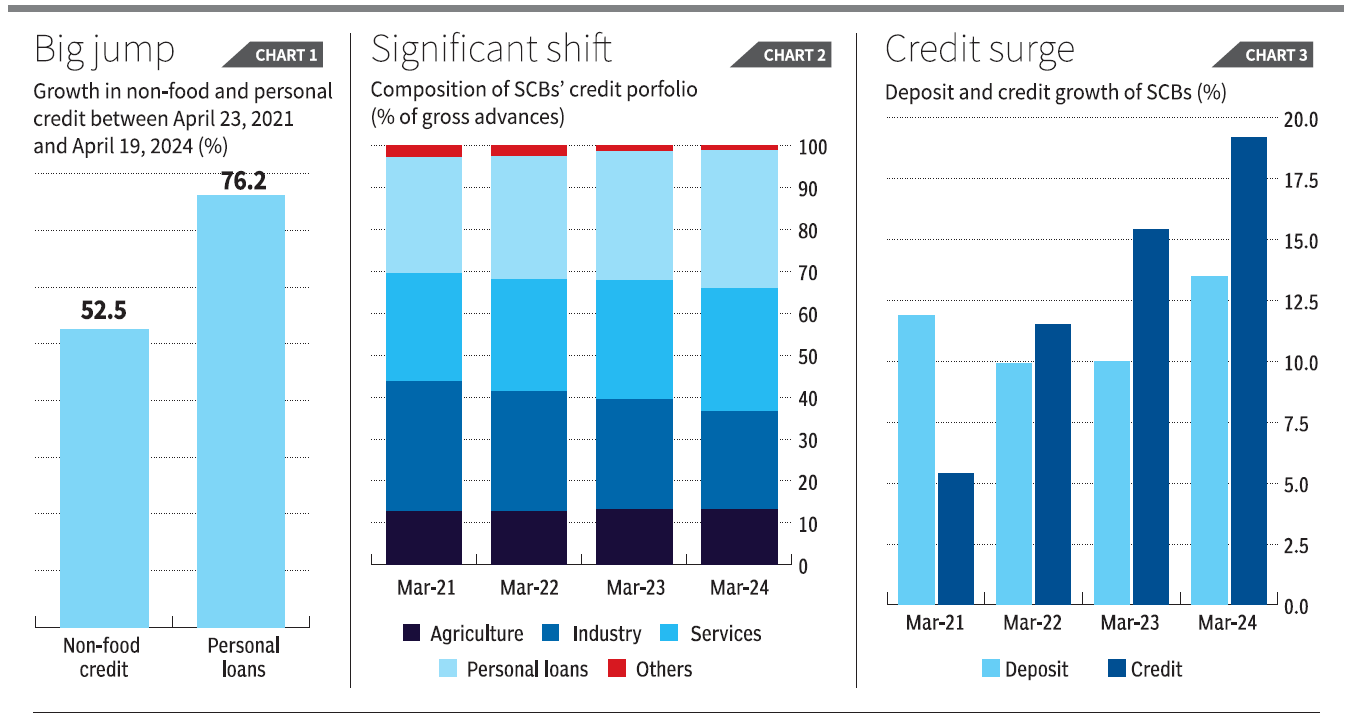

As Chart 1 shows, between late April 2021 and late April 2024, personal credit growth (76 per cent) outstripped the growth in non-food credit (53 per cent) advanced by scheduled commercial banks (SCBs) in India.

As Chart 1 shows, between late April 2021 and late April 2024, personal credit growth (76 per cent) outstripped the growth in non-food credit (53 per cent) advanced by scheduled commercial banks (SCBs) in India.

Personal loans consist predominantly of credit for housing (49 per cent of outstanding loans as of March 2024) and vehicle purchases (11 per cent), with credit card receivables and education loans amounting to around 4.9 and 2.3 per cent, respectively, of outstanding advances.

But a nebulous category identified as “other personal loans” accounts for a third of the total. These are possibly loans provided without a link to targeted assets like real estate or automobiles, which serve as the collateral for those asset-linked loans. That increases the potential loss in case of a default.

The result of the retail credit spike has been a significant shift in the composition of gross advances of the SCBs over the last three years. Over that short period, the share of personal loans in total advances has risen from 27.8 per cent at the end of March 2021 to 32.9 per cent at the end of March 2024 (Chart 2). This was also a period in which annual credit growth has accelerated, with credit growth exceeding deposit growth in the last three years (Chart 3).

The result of the retail credit spike has been a significant shift in the composition of gross advances of the SCBs over the last three years. Over that short period, the share of personal loans in total advances has risen from 27.8 per cent at the end of March 2021 to 32.9 per cent at the end of March 2024 (Chart 2). This was also a period in which annual credit growth has accelerated, with credit growth exceeding deposit growth in the last three years (Chart 3).

Rapid increases

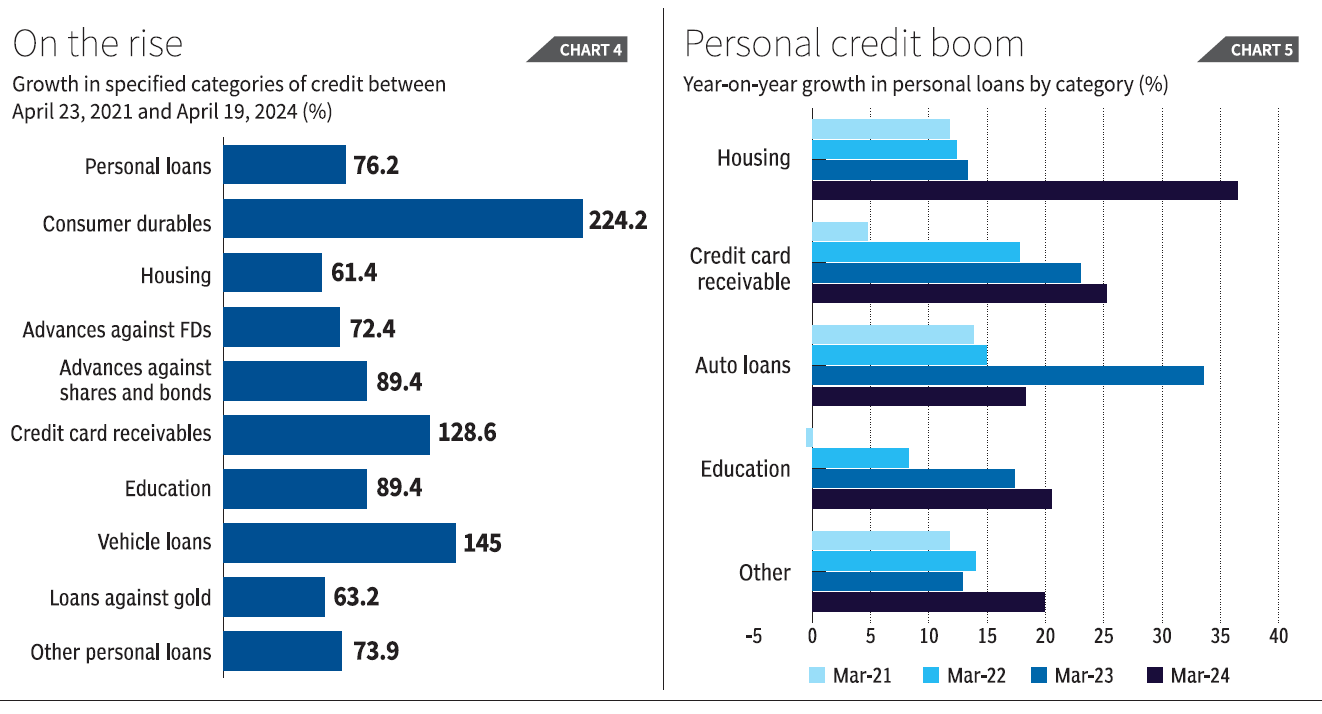

An assessment of more granular data suggests that personal credit in areas that till now have accounted for a small proportion of total outstanding personal loans, have been registering rapid increases over the last three years. The fastest growing sectors have been lending for purchases of consumer durables and vehicles, and credit card receivables, all of which have outstripped even the increase in personal loans (Chart 4). What is noteworthy is that “other personal loans” that account for a third of the total have also increased by 74 per cent.

Finally, the figures on the annual growth in personal credit by category points to an acceleration in the provision of loans under all heads (other than auto loans, which after sharp acceleration, slowed down in the 2023-24) (Chart 5).

There can be no doubt that we are witnessing the advance of a personal credit boom. It is true that increases in personal credit provision became the norm after financial liberalisation, which allowed and encouraged banks to lend for purchases for which the purchased asset or durable was the collateral, and then to lend against personal guarantees. This was considered safe, not only because thus far non-performing loans in the personal loan category have not been high, but also because liberalisation allowed for these loans to be securitised and traded, so that credit risk can be transferred, reducing the risk carried by the creator of the credit assets. But there is cause for concern in the evidence of “credit swings” that focus credit provision on certain sectors, reducing the degree of portfolio diversification. In the credit boom that occurred in the years after 2004, banks awash with liquidity swung in favour of provision of credit to corporates for large infrastructural investments in areas such as power generation and distribution, roads, ports and civil aviation. That trend, encouraged by neoliberal policy, led to a huge build-up of non-performing assets, much of which had to be written off, requiring repeated rounds of recapitalisation of the public sector banks by the government.

Retail lending favoured

With that experience having reduced the inclination of the banking community for infrastructural lending, the swing now seems to be in favour of retail lending. The problem with a retail credit boom is that sustaining it requires diversifying away from ‘safe’ areas like housing, to lending to support purchases of automobiles and durables, unspecified spending desires and credit card outstandings. These offer less robust or no collateral, increasing potential loss in case of default. Sustaining the retail boom also requires substantially increasing and widening the universe of borrowers, bringing in smaller borrowers who are more likely to face circumstances that precipitate default.

A recent Financial Stability Report of the RBI flags an increase in the share retail loans in the addition to or emergence of new bad loans. It also flags an increase in delinquencies or loans with early evidence of overdue payments among small borrowers who have borrowed less than ₹50,000. (See Datapoint by Vignesh Radhakrishnan in The Hindu (July 3, 2024) for a summary of the evidence.)

Of course, these are just early signs. But given the appetite for increased lending on the part of the SCBs, and the government’s tendency to encourage lending to hold up demand that is depressed by its own fiscal conservatism, credit provision must rise. As of now bankers are seeing the retail sector as the best to swing towards. But if the incipient signs of fragility in the retail sector lead to a spike in the volume of delinquent loans, the retail credit boom may well turn into a retail credit bubble.

_______________________________________

Courtesy: Business lines dt 9.7.2024